India hit E20 last year. Union minister Nitin Gadkari now wants E100. In late April 2026, the road transport ministry reportedly issued draft rules to recognise E85 and E100 vehicles under the Central Motor Vehicles Rules.

E20 hides the land question inside a 20% blend. E100 strips the camouflage off. It is no longer a small petrol tweak. It is a plan to run India’s transport on crops.

If the acre is treated as free, ethanol looks clean. If the water is free, it looks rural-friendly. If fertilizer, irrigation power, and distillery energy are background noise, it looks like a clever petrol substitute. None of those things are free.

So follow the acre.

TL;DR

- India is at ~20% ethanol blending today. Gadkari wants 100%. April 2026 draft rules add E85/E100 vehicle certification.

- Energy-equivalent E100 would need ~36.8 million acres of cane-equivalent land — roughly the area of Odisha — and ~244 km³ of water a year. That is ~half the Ganga’s annual flow, every year.

- Cane ethanol’s “biofuel” energy is 73% fossil input by the time you count irrigation pumps and fertilizer.

- E20 has 6.8% less energy per litre than petrol. The pump still says litre. Your engine pays the difference.

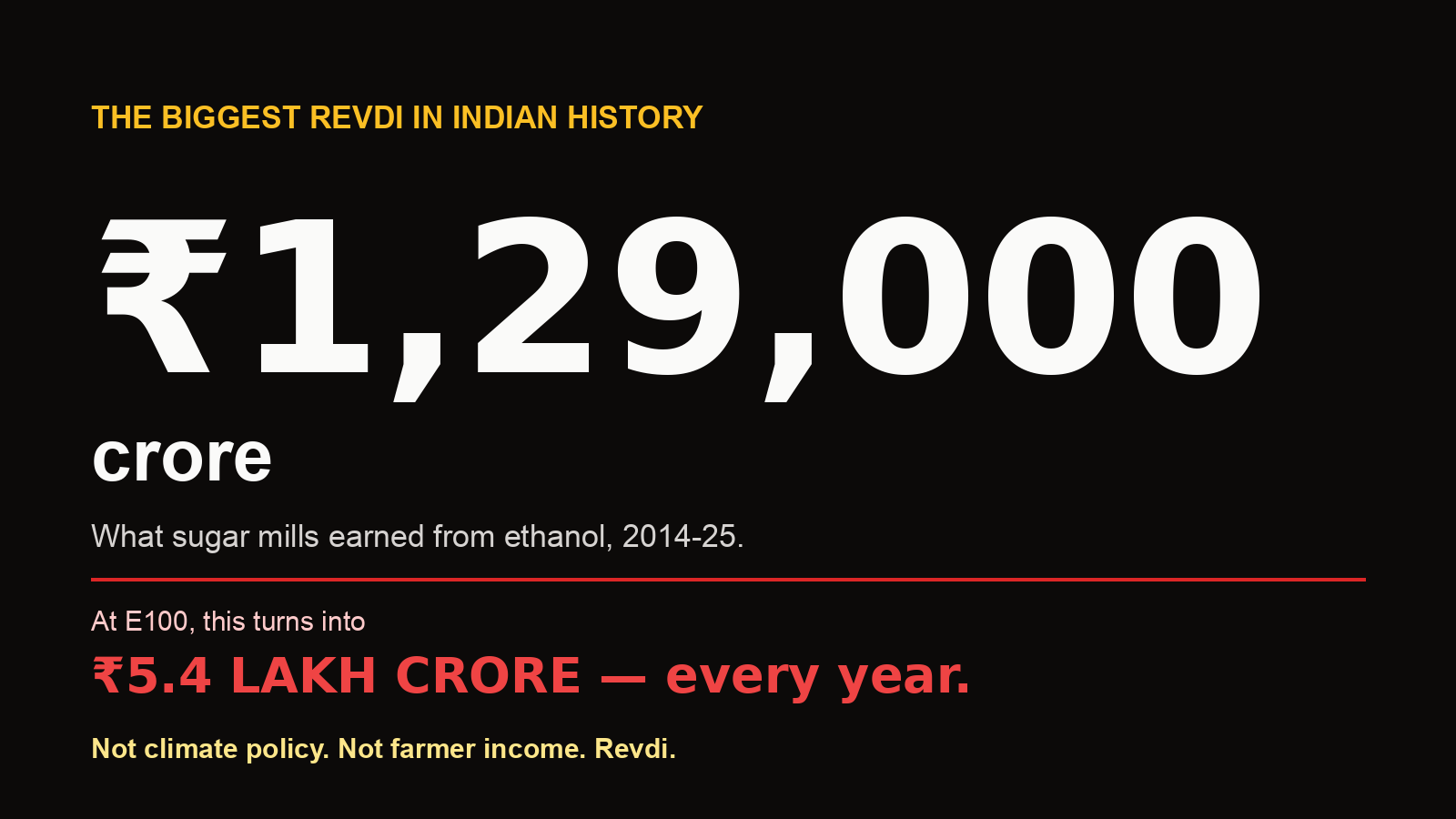

- E20 already moves ~₹70,000 crore/year to ethanol suppliers. E100 would move ~₹5.4 lakh crore/year. Listed sugar majors now treat ethanol as a strategic growth segment.

- One acre of solar feeding EVs delivers ~80x the vehicle-distance that one acre of cane delivers via ethanol’s petrol displacement. Per kilometre, EV-on-residential-electricity costs ~5x less than E20 at the pump.

- The land already growing E20 ethanol could electrify every petrol vehicle in India ten times over. About 10% of it is enough — only ~460,000 acres of solar. The other 90% goes back to food.

- The counterfactual is not petrol. It is electrons, food, and water.

E100 is not a tweak. It is a state-sized field.

Replacing India’s petrol with ethanol takes cane on a footprint the size of Odisha.

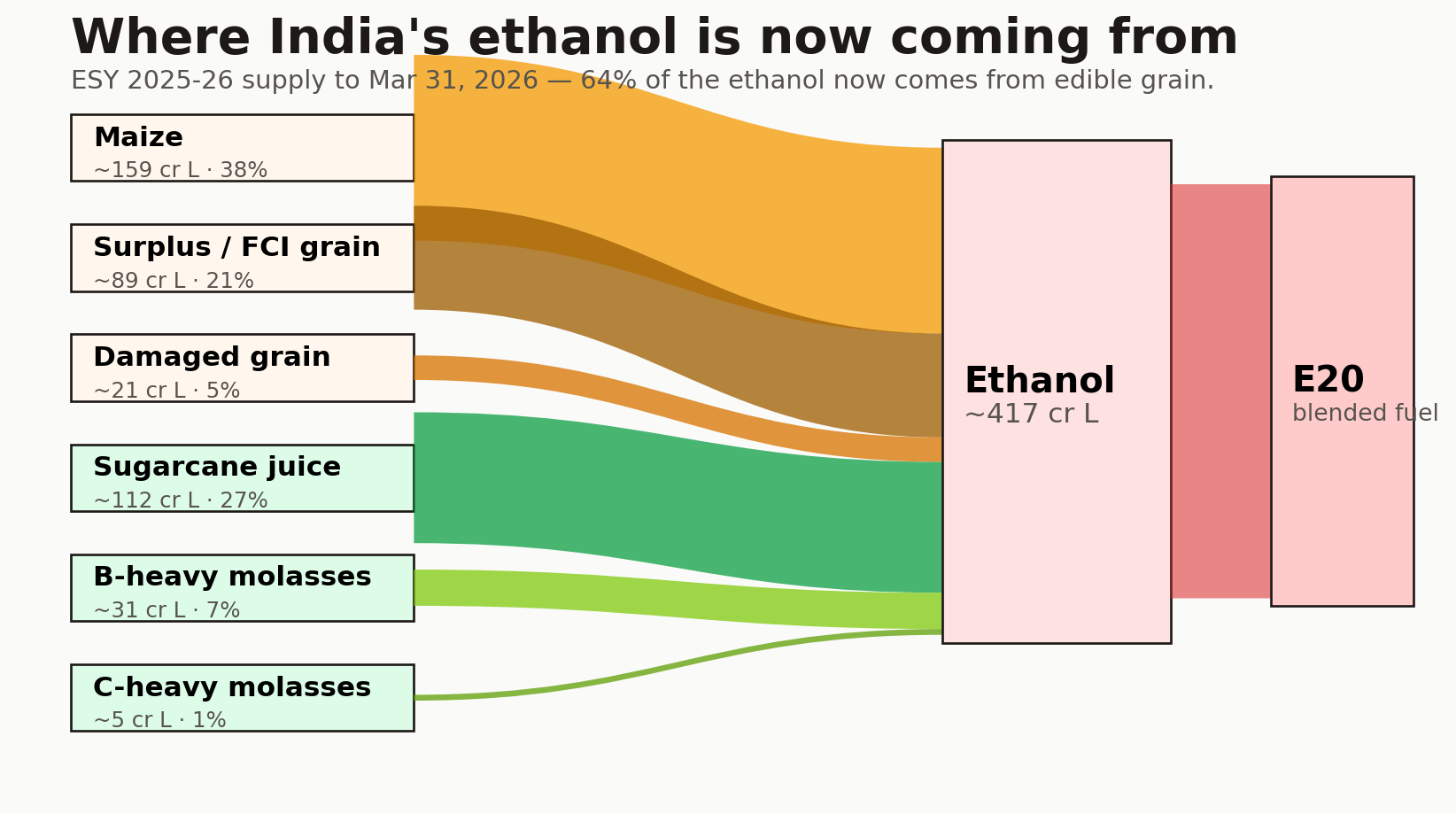

In ESY 2024-25, public-sector oil marketing companies achieved 19.24% ethanol blending. For ESY 2025-26, blending has been around 20%. By March 31, 2026, ethanol supply had reached about 417 crore litres, against roughly 1,050 crore litres allocated for the year. This is no longer a pilot.

Now imagine the next step Gadkari has named.

India’s FY25 petrol consumption was about 39.95 million tonnes at a density of ~0.745 kg/litre — about 53.6 billion litres of petrol. Petrol holds ~32 MJ/litre. Ethanol holds ~21.1 MJ/litre. Replacing petrol energy with ethanol therefore needs:

53.6B L × 32/21.1 = ~81.3B L ethanol = ~8,132 crore L/year

For context, today’s E20 demand is ~1,050 crore litres. India’s total ethanol capacity is ~1,950–2,000 crore litres. E100 is a different planet.

NITI’s roadmap uses ~70 L of ethanol per tonne of cane and ~31.58 tonnes of cane per acre — about 2,211 L of ethanol per acre per year. So energy-equivalent E100 from sugarcane needs:

81.3B L ÷ 2,211 L/acre = ~36.8M acres

That is ~149,000 km². Almost Odisha.

The water bill, at ~3,000 L of water per L of cane ethanol, is ~244 km³ per year.

Your fuel pump is eating from the ration shop

Ethanol is no longer mostly sugarcane. Maize and FCI grain now do most of the work — grain that hungry households need.

The lazy version of the story is “sugarcane is being turned into petrol.” The real version is worse.

| Feedstock | ESY 2025-26 supply to Mar 31, 2026 | Share |

|---|---|---|

| Maize | ~159 cr L | ~38% |

| Surplus / FCI grain | ~89 cr L | ~21% |

| Damaged grain | ~21 cr L | ~5% |

| Sugarcane juice | ~112 cr L | ~27% |

| B-heavy molasses | ~31 cr L | ~7% |

| C-heavy molasses | ~5 cr L | ~1% |

Sixty-four percent of India’s ethanol now comes from edible grain — maize, FCI rice, “damaged” grain — not from sugar mills’ byproducts. Sugarcane is the clearest water villain. Rice is often worse — paddy uses more groundwater per kg than cane. Maize is better than rice and often better than cane. None of them are free. Moving the feedstock does not remove the question. It just shifts which farmer, which aquifer, and which ration shop sits in the fuel chain.

E100 would drink half the Ganga, every year

Each litre of cane ethanol takes ~3,000 litres of mostly-groundwater. At E100 scale, that is half a Ganga annually.

The pump shows fuel litres. It does not show groundwater litres.

NITI cites water-use estimates of 2,860–3,000 litres of water per litre of ethanol from sugarcane, and a sugarcane water number of about 6,632 m³/acre/year.

Using 3,000 L water per L ethanol:

| Scenario | Ethanol | Water footprint |

|---|---|---|

| Current sugar-based ethanol | ~293 cr L | ~8.8 km³/year |

| E20 cane-equivalent | ~1,050 cr L | ~31.5 km³/year |

| E100 energy-equivalent | ~8,132 cr L | ~244 km³/year |

For scale: the Ganga’s annual flow at Farakka is ~459 km³. E100’s water demand from cane alone would be roughly half the Ganga, every year. It is more than the Krishna, Yamuna, and Cauvery combined. Most of it would come from groundwater that is already overdrawn.

Switching to maize lowers the per-litre water use but does not exit the problem. Rice ethanol is worse than cane. When fuel policy shuffles between cane, maize, rice, and damaged grain, you are not leaving the water question. You are choosing which aquifer to drain.

The food we choose not to grow

The acre is literal. The water is literal. The calories are literal.

India still has about 172 million undernourished people per SOFI 2025. India has the world’s largest child-wasting burden — roughly 21 million wasted children under five. About 42–43% of Indians cannot afford a healthy diet.

Yes, hunger is not solved by grain alone. It is income, storage, distribution, sanitation, gender, disease, purchasing power, and state capacity. India can have overflowing FCI godowns and persistent malnutrition at the same time, and does.

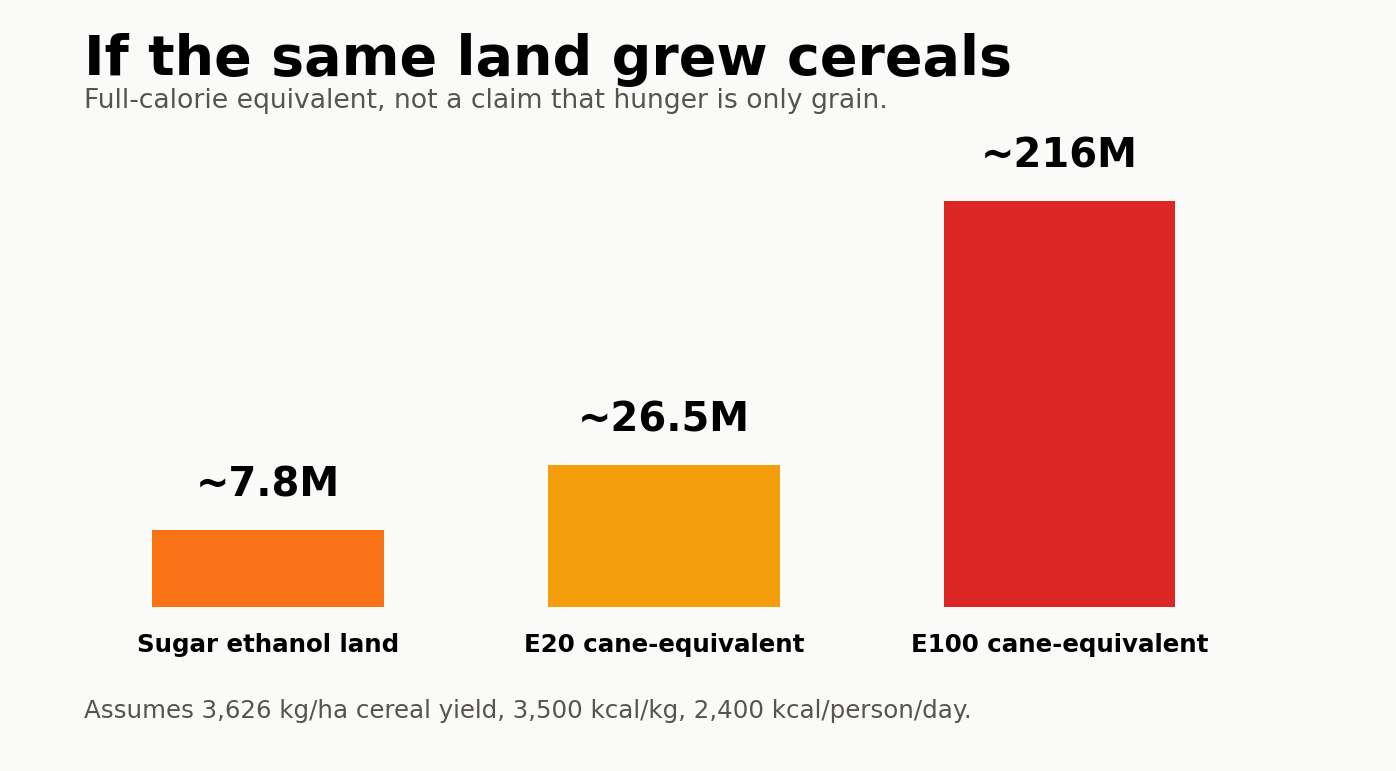

But the acre is literal. India averages ~1,468 kg of cereals per acre per year. At ~3,500 kcal/kg and a 2,400 kcal/person/day full-calorie benchmark, one acre of cereals can feed ~5.9 people for a year.

| Land counterfactual | Cane-equivalent land | Cereal calorie equivalent |

|---|---|---|

| Current sugar-based ethanol | ~1.33M acres | ~7.8M people/year |

| E20 cane-equivalent | ~4.52M acres | ~26.5M people/year |

| E100 energy-equivalent | ~36.8M acres | ~216M people/year |

Ethanol does not pull a child’s plate at the petrol pump. But the land-use choice is large enough to register against India’s hunger numbers. E100’s land alone could full-calorie-feed more people than India currently has undernourished.

The “biofuel” that runs on diesel and fertilizer

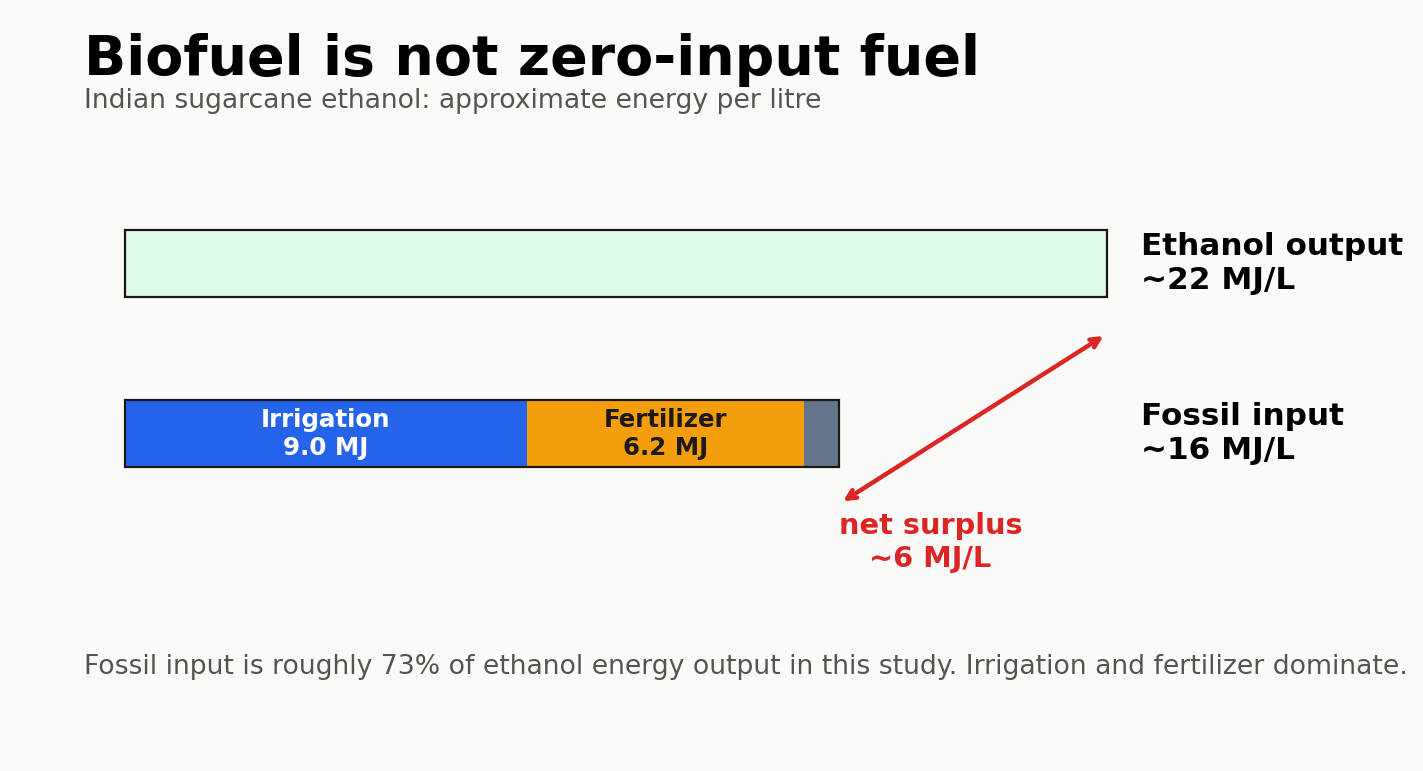

73% of an ethanol litre’s energy is fossil input — irrigation pumps and fertilizer plants in disguise.

Biofuel sounds like the opposite of fossil fuel. In India, the boundary is much messier.

A peer-reviewed net-energy analysis of Indian sugarcane ethanol estimates ~22 MJ of ethanol output per litre against ~16 MJ of fossil input — fossil input is ~73% of ethanol energy out. The net surplus is only ~6 MJ/litre.

| Input | Share of fossil input |

|---|---|

| Irrigation | ~56% |

| Fertilizer | ~39% |

| Farm operations and transport | small but non-zero |

This is why India is not Brazil. Brazilian cane ethanol borrows credibility from a different agronomic system. Indian cane sits on top of subsidised power, stressed groundwater, fertilizer factories, and politically protected cropping patterns. Calling it “renewable” is doing a lot of work with the “ish”.

The litre got smaller. You pay the difference.

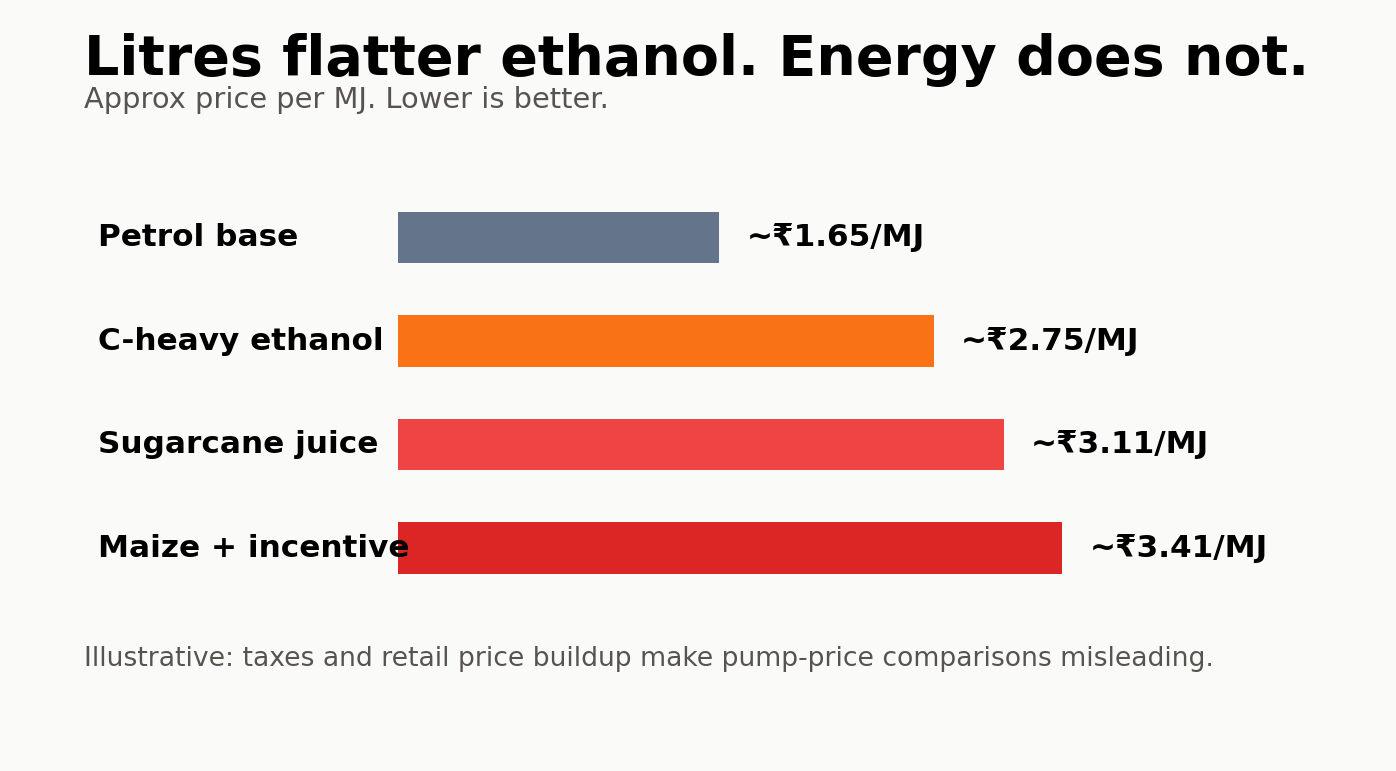

E20 has 6.8% less energy per litre than petrol. Older engines lose more. The pump still says litre.

A litre is a container, not a unit of usefulness. Ethanol puts less energy in the container.

| Fuel | Approx energy |

|---|---|

| Petrol | ~32.0 MJ/L |

| Ethanol | ~21.1 MJ/L |

| E20 | ~29.8 MJ/L |

E20 has 6.8% less energy per litre than pure petrol. Modern, optimised engines claw back some of that via ethanol’s higher octane. Older two-wheelers, used cars, and any pre-E20 engine cannot. They quietly lose mileage, gain corrosion risk on rubber and aluminium parts, and drift outside warranty assumptions written for E10 fuel.

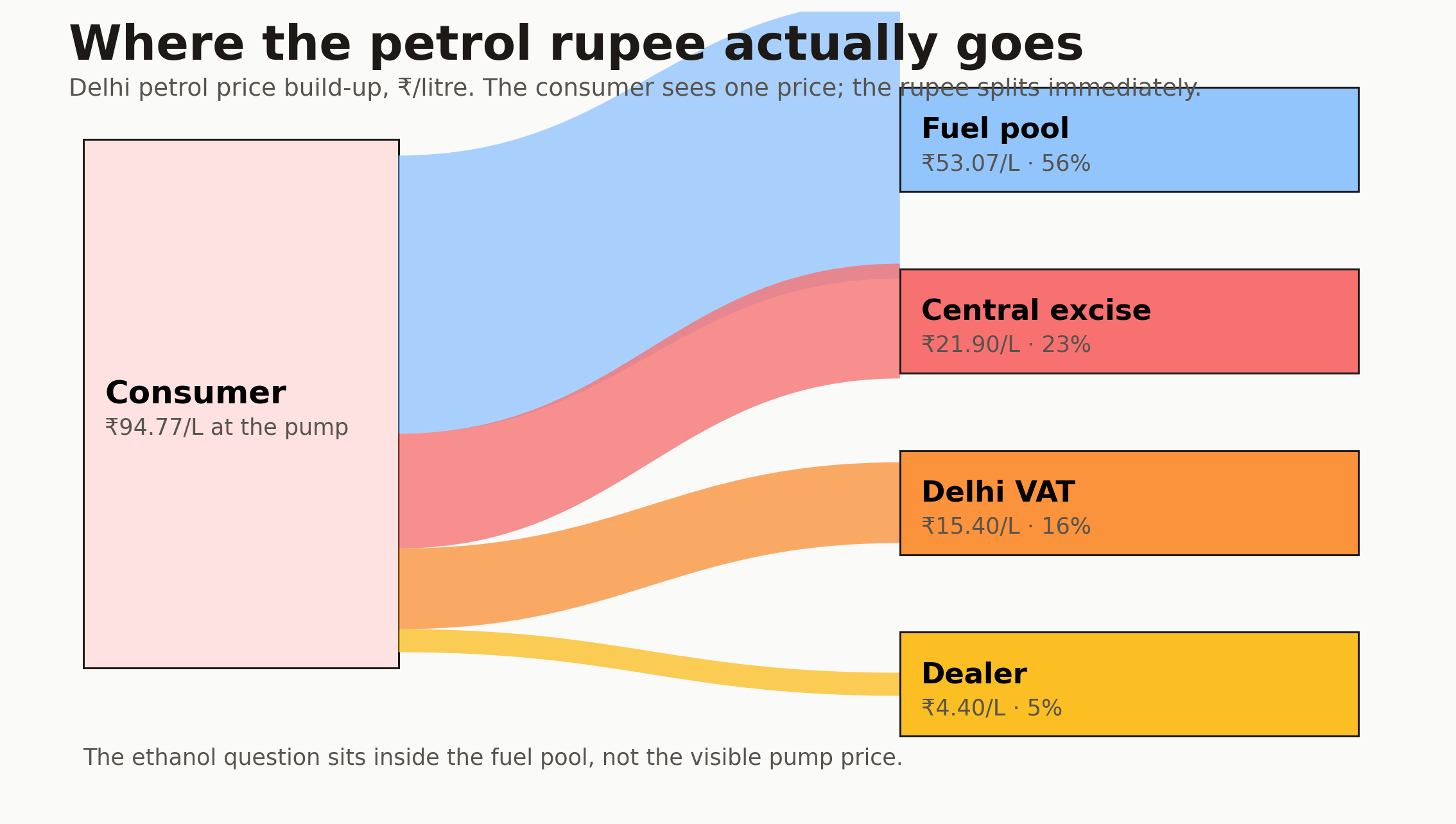

The rupee comparison is also rigged in ethanol’s favour. Procurement prices for ESY 2025-26 are ~₹58–66/L. Delhi retail petrol is ~₹95/L — but that includes ~₹37/L of central excise, VAT, and dealer commission. Pre-tax petrol is much cheaper than the pump suggests. Adjust for energy content and ethanol stops looking like a bargain.

The pump says litre. The engine consumes energy. The road consumes kilometres. Two of those three are silently shrinking.

₹70,000 crore a year, flowing to distilleries

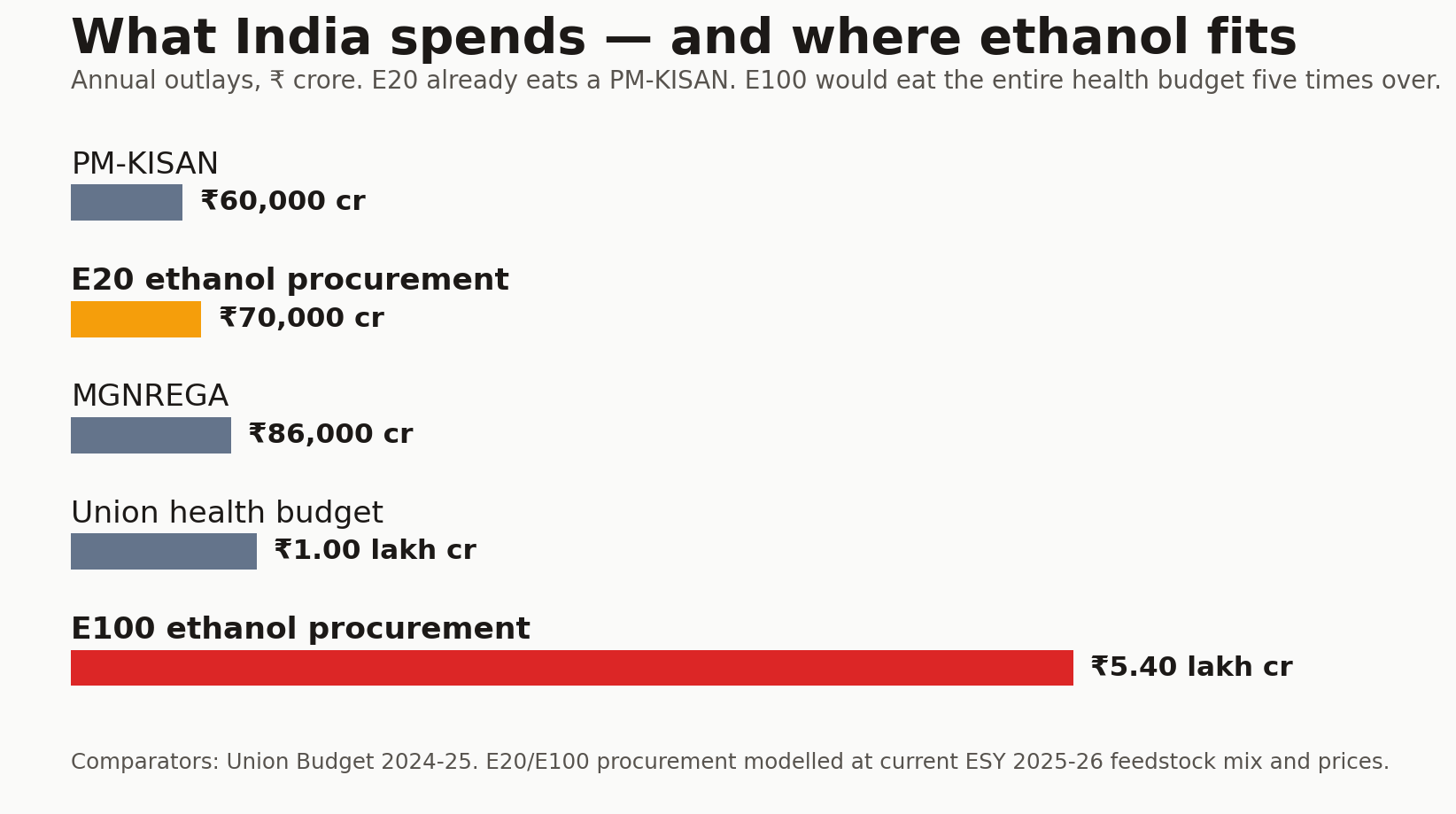

E20 already moves ₹70K cr/year. E100 would move ₹5.4 lakh crore/year. That is the prize being chased.

Start with the rupee the consumer hands over. In Delhi, most of the petrol pump price is tax and dealer commission before you ever get to the fuel pool.

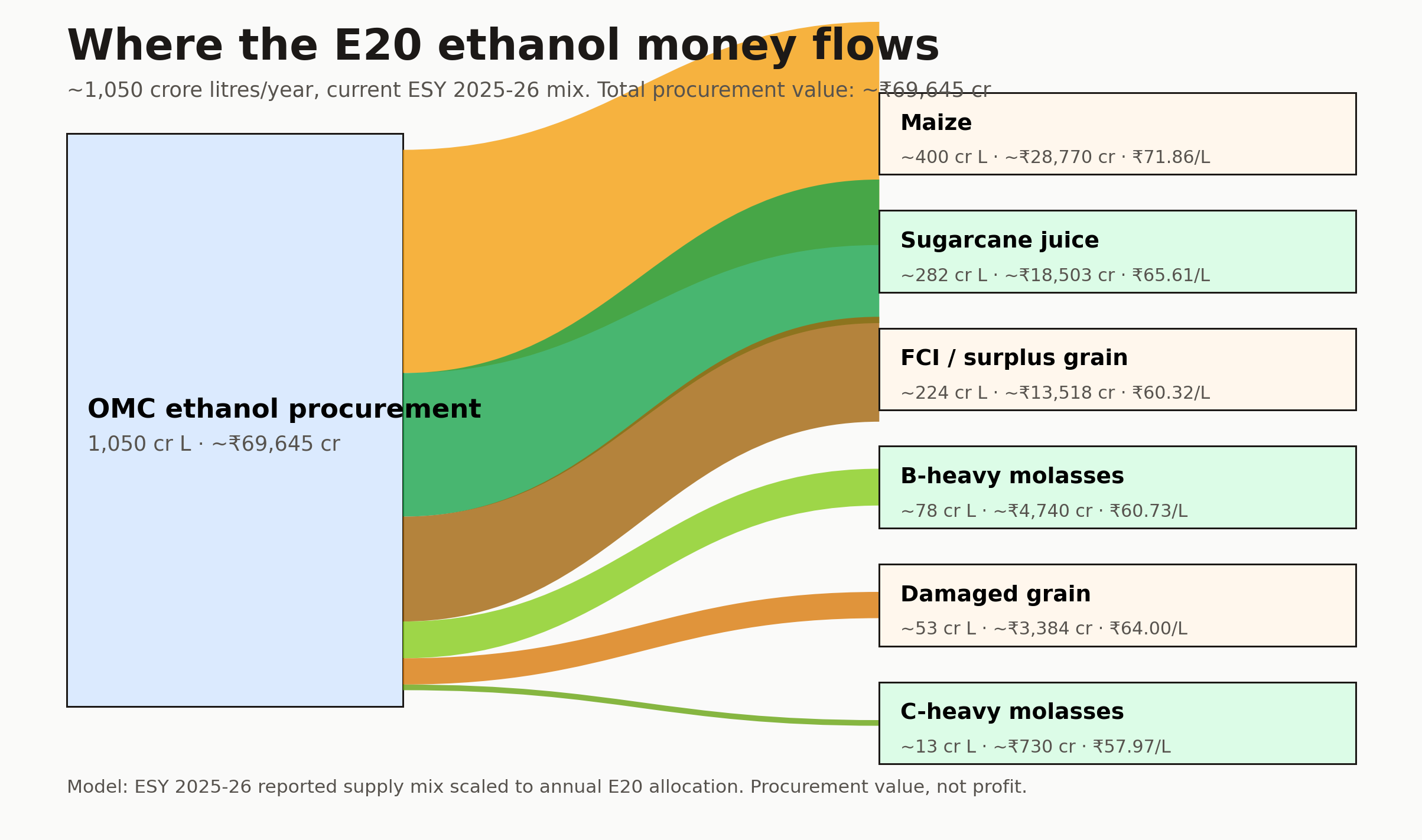

Inside the fuel pool sits ethanol. Using the current ESY 2025-26 supplied feedstock mix scaled to ~1,050 crore litres of E20 allocation, OMCs are moving roughly ₹69,600 crore/year into ethanol suppliers.

Notice that maize sits at the top of the procurement chart at ~₹71.86/L — the highest per-litre price of any feedstock, above sugarcane juice (₹65.61/L) and well above molasses (₹58–61/L). That is not a market price; CCEA fixes a different rate for each feedstock to push capacity in the direction it wants. See the FAQ below for why maize is priced highest.

That number lands somewhere in the company of India’s largest welfare programmes. E100 would put it past the entire Union health budget.

| Annual outlay | ₹ crore/year |

|---|---|

| PM-KISAN | ~60,000 |

| MGNREGA | ~86,000 |

| Union health budget | ~1,00,000 |

| E20 ethanol procurement | ~70,000 |

| E100 ethanol procurement | ~5,40,000 |

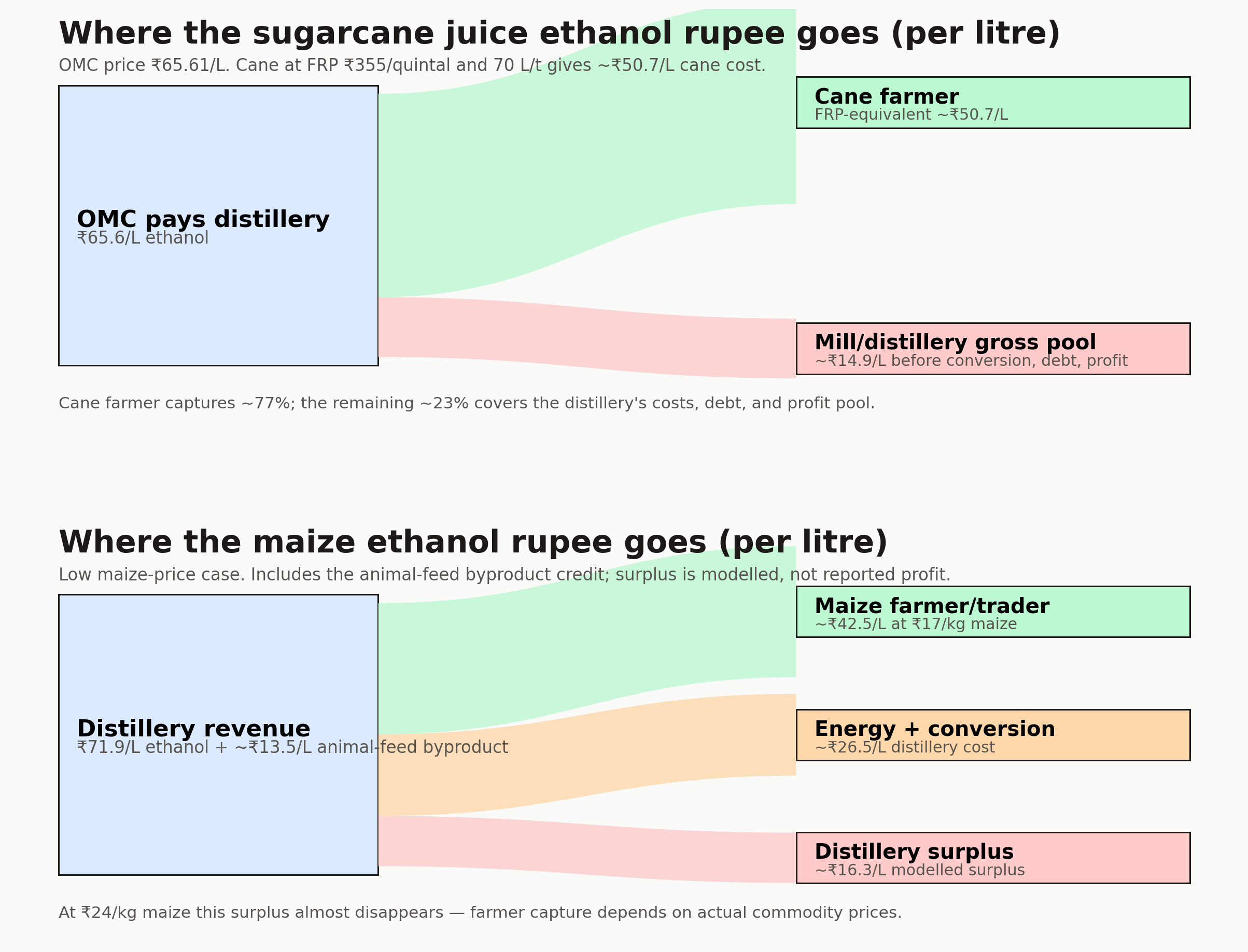

For sugarcane juice ethanol at the OMC procurement price of ₹65.61/L, with cane at the 2025-26 FRP of ~₹355/quintal and 70 L ethanol/tonne cane, the cane itself costs about ₹50.7/L of ethanol. The mill/distillery gross pool is about ₹14.9/L before conversion cost, capex, debt, and profit. Maize ethanol can be more profitable still, especially in low-maize-price years when the animal-feed byproduct (the spent grain after fermentation) is sold alongside.

The biggest revdi in Indian history

Sugar mills made ₹1,29,000 crore from ethanol in a decade. E100 would turn that into ₹5.4 lakh crore — every single year.

If this were just farmer support, listed sugar and distillery companies would not be talking about ethanol as their growth story. They are.

| Company | Public disclosure | What it shows |

|---|---|---|

| Triveni Engineering | FY25 annual report positions Triveni among India’s largest integrated sugar and ethanol manufacturers; FY23 alcohol revenue was ~₹1,172 cr with PBIT ~₹212 cr | Alcohol/ethanol is a major segment, not a footnote |

| Balrampur Chini | FY24 distillery revenue ~₹1,425 cr | Distillery is a large recurring line |

| Dalmia Bharat Sugar | FY25: ethanol/distillery contributed ~28% of total revenue | Ethanol is strategically central |

| Bajaj Hindusthan Sugar | FY25 distillery revenue ~₹705 cr | Even weaker sugar firms have meaningful distillery revenue |

| EID Parry | FY25: distillery revenue improved; profitability hit by policy/feedstock changes | Policy moves distillery economics directly |

| Praj Industries | Q1 FY26: domestic ethanol-market caution after E20 weighed on performance | Equipment vendors also need ethanol momentum |

Connect the three things. Ethanol is now a strategic growth segment for listed sugar majors. The cheque flowing to distilleries goes from ~₹70,000 crore to ~₹5.4 lakh crore in the move from E20 to E100 — about an 8x increase. The minister keeps publicly aspiring to E100. None of those facts are surprising. They are aligned.

The word “ethanol” is doing four jobs at once: oil-import reduction (partly true at the margin), farmer income support (politically true), sugar-surplus management (very true), and climate mitigation (the weakest, once land, water, fertilizer, irrigation, distillation, and the solar opportunity cost enter the model). If the goal is sugar-sector working capital, call it that. Call the rest what it is: the biggest revdi in Indian history, paid quietly inside the petrol pump while the consumer pays in mileage, engine wear, water, and a fuel system the government itself is preparing to mutate.

One acre, two energy systems

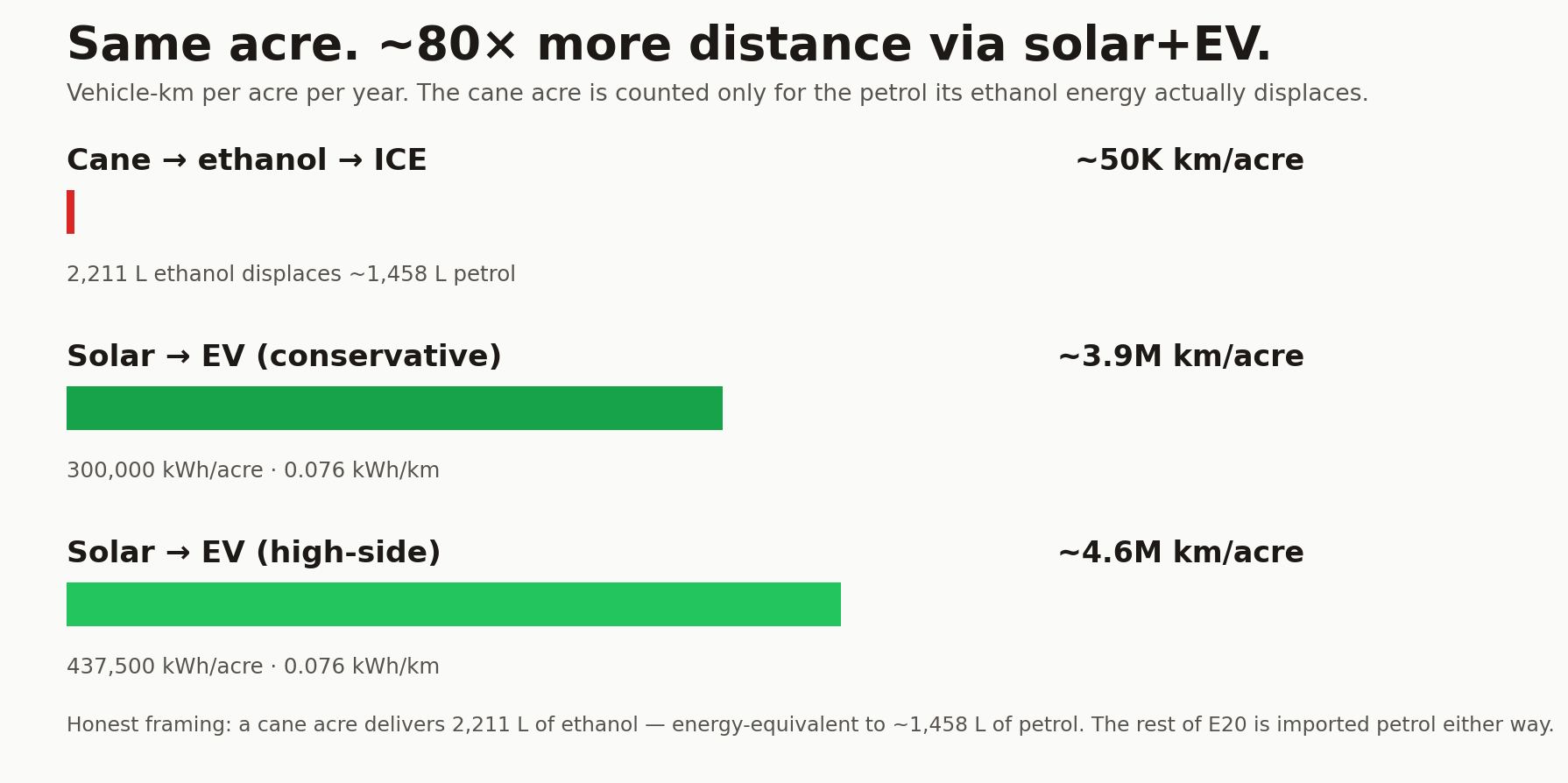

Cane ethanol displaces ~50K vehicle-km of petrol per acre per year. Solar feeding EVs delivers ~4M EV-km on the same acre. ~80x.

The honest comparison is not “cane → blended E20 fuel → distance” — that gives the cane acre credit for the petrol it gets blended with. The honest comparison is what each acre actually contributes.

The ethanol acre

Use NITI’s sugarcane assumptions:

| Step | Value |

|---|---|

| Cane yield | 31.58 tonnes/acre |

| Ethanol yield | 70 L/tonne cane |

| Ethanol output | 2,211 L/acre/year |

| Energy in that ethanol | ~46.7 GJ/acre/year |

| Petrol that energy displaces | ~1,458 L/acre/year |

| ICE vehicle-km from displaced petrol (~34 km/L) | ~49,600 km/acre/year |

That is the acre’s actual contribution to vehicle-distance. The remaining 80% of the E20 fuel still comes from oil refineries.

The solar acre

Now put utility solar on the same acre.

| Step | Value |

|---|---|

| Solar land use | 4–5 acres/MWdc |

| Annual generation per MW | ~1.4–1.75 M kWh/year |

| Annual electricity per acre | ~280,000–437,500 kWh (use 300,000 conservative) |

| EV consumption (weighted India petrol-vehicle mix) | ~0.076 kWh/km |

| EV-km per acre | ~3.9–4.6 million km/acre/year |

Same acre. ~80x the distance.

We don’t need new land. We don’t even need most of the land we already use.

The cane already feeding E20 could electrify every petrol vehicle in India ten times over. About 10% of it is enough; the other 90% goes back to food.

Stack the per-acre comparison up to the full Indian fleet.

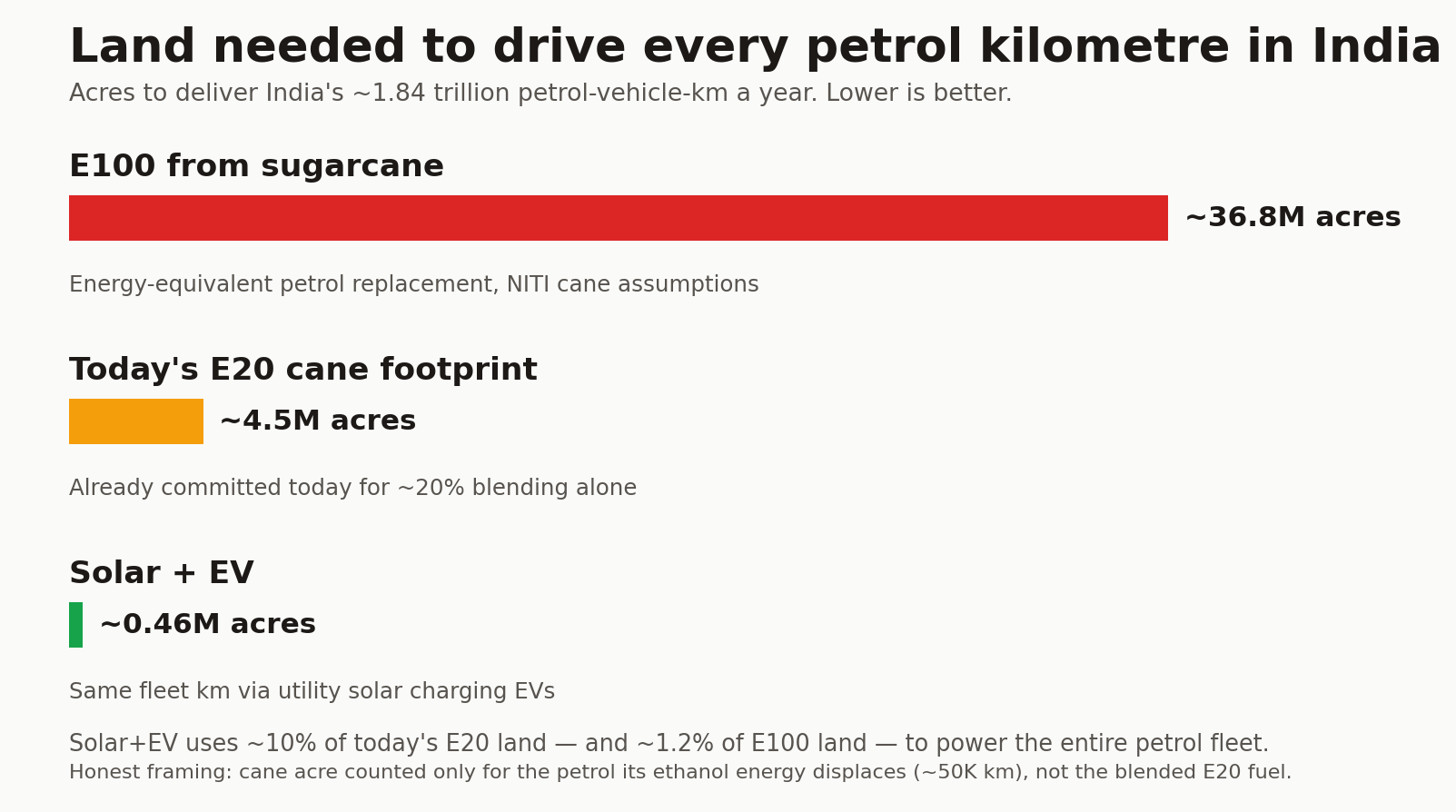

India’s petrol vehicles consume ~53.6 billion litres of fuel a year. At a weighted ~34 km/L across the petrol-vehicle mix, India’s petrol vehicles together travel about 1.84 trillion vehicle-km/year.

Now look at what the land already growing E20 ethanol could do if it were solar instead.

- E20’s cane-equivalent footprint today: ~4.5 million acres.

- At ~4 million EV-km per acre per year of utility solar: ~18 trillion EV-km/year.

- That is ~10 times every petrol-vehicle kilometre driven in India.

Turn it the other way around. To electrify the entire Indian petrol fleet via solar+EV needs only:

1.84T km ÷ 4M km/acre = ~460,000 acres

That is about 10% of the land we already grow E20 ethanol on. Or about 1.2% of the land E100 would need. The other 90–99% of the land goes back to food, forest, fallow, or rest.

It is also cheaper per kilometre, even comparing retail to retail.

| Pathway | Cost per km |

|---|---|

| EV km on residential electricity (~₹8/kWh × 0.076 kWh/km) | ~₹0.61/km |

| Petrol km at the pump (~₹95/L ÷ ~32 km/L on E20) | ~₹2.97/km |

Solar+EV at residential rates delivers each kilometre at roughly one-fifth the pump cost. Charge from your own roof at near-zero marginal cost and the gap widens further.

In total annual rupees, electrifying every petrol-vehicle kilometre via utility solar costs about ₹4.1 lakh crore/year in electricity (138 billion kWh × ₹3/kWh wholesale). India’s E100 ethanol procurement alone — before petrol-pump taxes, refinery margins, or anything else — would cost about ₹5.4 lakh crore/year. The cleaner pathway is also the cheaper one.

Petrol on EMI = kabaad on EMI

Remember what happened to BS-IV diesels in 2020? Now imagine BS-VI petrol when E85 pumps roll in.

Anyone who bought a BS-IV diesel in 2018 or 2019 remembers what came next. BS-VI norms rolled in on April 1, 2020. Resale collapsed. Used-car listings stopped moving. Fleet operators dumped vehicles into the kabaadi market. The vehicle did not stop working. It stopped being valuable.

A new petrol vehicle bought in 2026 sits on the same trajectory. The minister has publicly named E100. Draft rules already recognise E85 and E100 vehicles. Once E85 pumps appear at any scale, today’s BS-VI petrol moves into the BS-IV category. The fuel pump availability, the warranty assumptions, the resale market — all of it gets repriced under your feet.

If you buy a petrol vehicle after reading this, you must be crazy. You are signing a 7-year EMI on a fuel system the government itself is publicly trying to mutate. You will pay roughly 5x more per kilometre than an EV would cost. Your resale value is a bet on which side of the E85/E100 transition you exit. And every rupee in your fuel bill is bankrolling a ₹5 lakh crore revdi to sugar mills and grain distilleries — paid in water India does not have, in grain hungry households need, and in mileage your engine quietly loses.

The next vehicle ends the bet. Charge from your roof, from your housing society’s terrace solar, or from the grid at residential rates. Per kilometre, you spend a fifth. You stop sending water into a distillery. You stop bankrolling the revdi. And you remove the political-economy lever that makes E100 attractive to people who are not you.

What India should do instead

Cap E20. Price fuels honestly. Electrify two-wheelers fast. Stop calling all ethanol green.

- Cap E20. Do not sleepwalk into E85 or E100. The land-water-food arithmetic does not survive the scale.

- Publish monthly feedstock-level data. Cane juice, B-heavy, C-heavy, maize, FCI rice, damaged grain, and 2G ethanol — separately.

- Price and discuss fuels in ₹/MJ and km/acre, not just ₹/litre. A litre is a container, not a unit of usefulness.

- Stop labelling all ethanol “green”. Tag each batch by feedstock, water footprint, and fossil input.

- If the goal is farmer income, pay farmers directly. Or pay them for better land use: crop diversification, solar leasing, agrivoltaics where it works, and 2G residue ethanol where lifecycle accounting actually survives contact with reality.

- Electrify two-wheelers as fast as possible. That is the largest petrol-litre wedge in the country and the cheapest one to flip.

The counterfactual is not petrol. The counterfactual is electrons.

FAQ

If solar is 80x better, why is India doing ethanol at all?

Because each link in the chain has a local reason to keep it going. The farmer gets a buyer. The sugar mill gets liquidity. The distillery gets offtake. The OMC gets a compliance story. The government gets farmer-income politics, forex-savings optics, and a green-fuel narrative. Listed sugar companies get a strategic growth segment. The consumer gets a normal-looking petrol pump. Nobody in that chain is paying the water bill or the land-opportunity-cost bill. It is the biggest revdi in Indian history precisely because no single participant has to feel guilty for accepting their slice.

Will my old petrol vehicle become worthless?

Not overnight. But every step from E10 to E20 to E85 to E100 chips away at fuel availability for older blends, resale value, maintenance economics, and warranty assumptions. The BS-IV-to-BS-VI transition in 2020 is the right reference point. Vehicles did not stop running. They stopped being valuable. A new petrol vehicle bought in 2026 is a bet that this transition holds. An EV takes that bet off the table.

What about night driving and grid coverage for EVs?

Two-wheelers are the largest petrol wedge in India and almost always charge overnight at home. Solar+battery economics keep improving. Even on today’s grid, EV cost per km is well below petrol per km. Range and charging are real questions for long-haul cars, but they are not reasons to keep burning crops to move a scooter to work.

Is India’s ethanol mostly sugarcane?

Not anymore. Sugarcane remains politically and economically central, but current supply is increasingly grain-heavy, especially maize and surplus or FCI grain. About 64% of current ethanol is now from edible grain. That does not weaken the critique. It expands it from sugarcane ethanol to “the fuel pump is taking from the ration shop”.

Why does maize ethanol get ~₹71/L when sugarcane juice gets ~₹65/L?

Because it is a government-set procurement price, not a market price. CCEA fixes a different per-litre rate for each feedstock each ESY. Maize is priced higher than cane juice for three reasons:

- Higher conversion cost. Cane juice ferments directly. Maize needs an extra processing chain — milling → cooking to gelatinise the starch → enzymatic saccharification → fermentation → distillation. More steps, more energy, more capex. The premium is meant to cover that gap.

- Higher feedstock cost per litre. At ~₹17–24/kg maize and ~380–450 L of ethanol per tonne, the raw maize alone runs ~₹40–60/L of ethanol. Cane at FRP ₹355/quintal × 70 L/tonne is ~₹50/L. Similar order, but maize is more volatile and trades at open agri-commodity rates, so the procurement price has to clear above the swing.

- Capacity-build subsidy. The big policy push since 2020 has been to move ethanol away from sugarcane (water stress, sugar-mill dependence) and toward grain. Pricing maize ethanol at a clear premium incentivises distillers to build new grain or dual-feed capacity rather than just leveraging existing sugar mills.

The irony: maize ethanol also earns the animal-feed byproduct revenue (~₹13.5/L extra to the distillery), which would normally argue for a lower procurement price, not higher. The premium plus the byproduct credit is what makes maize the most attractive segment for distillery operators right now — and explains why “maize” sits at the top of the procurement Sankey at ~₹28,800 cr/year.

Does E20 reduce oil imports?

Yes, at the margin. But ethanol has lower energy density than petrol, so the energy displacement is smaller than the litre displacement. The relevant question is not “does it save some petrol?” It is “is this the best use of land, water, crop procurement, and policy attention?” Same land as solar saves an order of magnitude more.

Does E20 reduce mileage?

E20 has about 6.8% less energy per litre than petrol. Optimised engines can recover some efficiency through ethanol’s higher octane. Older or non-optimised vehicles see more visible mileage loss and additional corrosion risk on rubber and aluminium parts.

Is ethanol cheaper than petrol?

Compared to taxed retail petrol, sometimes. Petrol retail includes large central excise, VAT, and dealer commission. On a pre-tax, energy-adjusted basis, ethanol — especially grain ethanol — is not obviously cheap. EV-on-residential-electricity beats both, by ~5x per kilometre.

What is the E100 problem?

Scale. Replacing India’s petrol energy with ethanol needs about 8,132 crore litres/year of ethanol. From sugarcane, that is about 36.8 million acres of cane-equivalent land — roughly Odisha — and 244 km³ of water a year, about half the Ganga’s annual flow.

Can sugarcane land simply become solar?

Not everywhere, not instantly, and not without distributional issues. Some farmland is better suited to crops, some to solar, some to agrivoltaics, some to neither. But the marginal-acre comparison is honest. “Not every acre can convert tomorrow” is not a defence of pretending the opportunity cost is zero.

What about second-generation ethanol?

2G ethanol from residues is much more defensible in principle. It avoids the direct crop-to-fuel land conversion. But 2G has its own collection, logistics, and cost challenges, and it is not what is currently being scaled. The critique here is mainly first-generation crop ethanol.

How does the per-acre comparison get to ~80x?

Two numbers, each derived from the same acre.

Cane → ethanol → ICE. One acre yields ~31.6 tonnes of cane (NITI), which makes ~2,211 L of ethanol at 70 L/tonne. That ethanol holds ~46.7 GJ of energy — enough to displace ~1,458 L of petrol on an energy-equivalent basis. At the weighted Indian petrol-vehicle mileage of ~34 km/L, that is ~50,000 vehicle-km/acre/year. The acre is credited only with the petrol it actually displaces; the rest of the E20 blend is imported petrol either way.

Solar → EV. One acre of utility solar produces ~300,000 kWh/year (4–5 acres/MW × 1.4–1.75 M kWh/MW). At ~0.076 kWh/km for the same vehicle mix electrified, that is ~4,000,000 EV-km/acre/year.

Ratio: 4,000,000 / 50,000 ≈ 80x.

This triangulates with the underlying physics: solar gathers ~23x more raw energy per acre than cane→ethanol (1,080 GJ vs 46.7 GJ), and EVs convert that energy to motion ~3.4x more efficiently than ICE engines. 23 × 3.4 ≈ 80. Whatever assumptions you swap in, the ratio sits in the 75–115x range. The fleet-scale conclusion holds throughout: ~460,000 acres of solar covers every petrol vehicle in India.

What if the land grew food instead?

At India’s cereal yields, E100 cane-equivalent land could feed about 216 million people a full-calorie diet. Hunger is not only about grain, but the land-use choice is large enough to matter against India’s 172 million undernourished.

Should someone buy a petrol car now?

If the budget supports an EV at all, buy the EV. If it does not, buy used and small. A new ICE in 2026 takes a 7-year EMI on a fuel system the government itself is publicly trying to mutate. Tomorrow’s BS-IV.

Tweet drafts

The land-savings punchline:

India’s E20 ethanol already uses ~4.5 million acres of cane.

Put utility solar on the same land, charge EVs from it, and you can power every petrol vehicle in India 10x over.

Or use just 10% of it. The other 90% goes back to food.

Same acre, twin pathways:

Same acre.

Cane → ethanol → ICE: ~50,000 vehicle-km/year (just what the ethanol’s energy displaces from petrol).

Solar → EV: ~4,000,000 vehicle-km/year.

~80x more driving. ~5x cheaper per km.

The counterfactual is not petrol. It is electrons.

Revdi:

Sugar mills earned ₹1,29,000 crore from ethanol in a decade.

E100 would make it ₹5.4 lakh crore — every year.

This is not climate policy. This is the biggest revdi in Indian history, paid quietly inside the petrol pump.

Vehicle-buying:

A new petrol vehicle in 2026 = BS-IV diesel in 2019.

The minister himself is publicly aspiring to E100. E85/E100 draft rules already exist.

Petrol on EMI = kabaad on EMI.

Food shock:

India still has ~172 million undernourished people.

64% of India’s ethanol is now from edible grain — maize, FCI rice.

Your fuel pump is now eating from the ration shop.

Sources and notes

- PIB, Year End Review 2025: Ministry of Petroleum and Natural Gas, for ESY 2024-25 blending, capacity, and farmer-payment framing.

- PPAC, Petroleum Planning and Analysis Cell, for blending trackers and petrol/diesel demand.

- NITI Aayog, Roadmap for Ethanol Blending in India 2020-25, for cane-ethanol yield and water-use assumptions.

- PRS, Summary of NITI Aayog ethanol roadmap, for policy background.

- ChiniMandi, Ethanol supply hits 417 crore litres in ESY 2025-26, for March 31, 2026 feedstock supply.

- ChiniMandi, OMCs allocate around 1049 crore litres for ESY 2025-26, for contracted feedstock mix.

- PIB, FRP of sugarcane for sugar season 2025-26, for the ₹355/quintal cane price.

- NDTV/PTI, India should aim to achieve 100% ethanol blending: Nitin Gadkari, for the April 2026 E100 statement.

- Economic Times/PTI, India should aim for 100% ethanol blending, says Nitin Gadkari, for corroborating the E100 statement.

- Moneycontrol, Government notifies draft norms to include E85, E100 fuels, for the April 2026 draft-rule reporting.

- ETEnergyWorld, FY25 petrol consumption up 7.3%, for FY25 petrol consumption.

- ScienceDirect, Net energy analysis of sugarcane based ethanol production in India, for fossil-energy input shares.

- Kafila Agro, Maize-to-Ethanol Challenges, for the maize conversion-cost and DDGS byproduct model.

- Times of India, Rice industry hit as ethanol production shifts to maize, for reported low maize prices near ethanol demand centres.

- Triveni Engineering, Annual Report 2024-25, for sugar/ethanol positioning.

- Triveni Engineering, FY23 Alcohol Business disclosure, for alcohol revenue and PBIT.

- StockAnalysis, Balrampur Chini revenue by product, for distillery segment revenue.

- Dalmia Bharat Sugar, Annual Report 2024-25, for ethanol/distillery revenue contribution.

- StockAnalysis, Bajaj Hindusthan Sugar revenue by segment, for distillery segment revenue.

- EID Parry, Annual Report 2024-25, for distillery segment discussion.

- ChiniMandi, Praj announces Q1 FY26 results, for ethanol-market caution after E20.

- PPAC/CRISIL, All India study on sectoral demand of petrol and diesel, for petrol-use sector split underlying the weighted ~34 km/L petrol-fleet figure.

- World Bank, Cereal yield (kg per hectare) - India, for cereal-yield assumptions (converted to acres in this article).

- WHO, The State of Food Security and Nutrition in the World 2025, for SOFI 2025.

- United Nations in India, FAO presents the SOFI 2025 Report in New Delhi, for hunger framing.

- Drishti IAS, State of Food Security and Nutrition in the World 2025, for India-specific SOFI summary figures.

- MERCOM India, Solar PPA tariffs in recent auctions, for the ~₹3/kWh utility solar reference used in the cost-per-km comparison.

- CWC, Integrated Hydrological Data Book (Ganga basin), for Ganga annual flow at Farakka.

- Union Budget 2024-25 expenditure documents, for PM-KISAN, MGNREGA, and Department of Health and Family Welfare allocations used in the spend-comparison chart.

- CEA, CO2 Baseline Database for the Indian Power Sector, for grid-emissions context.